Healthcare coverage is one of the most important considerations for older adults and individuals who qualify for government-sponsored health insurance programs. In the United States, Medicare serves as a primary source of healthcare coverage for millions of people. However, many beneficiaries discover that there is more than one way to receive Medicare benefits, leading to a common question: What is the difference between Medicare Advantage and Medicare?

Understanding the distinction between Original Medicare and Medicare Advantage is essential because each option offers different benefits, costs, provider networks, and coverage structures. While both programs are designed to help cover healthcare expenses, they operate differently and may suit different healthcare needs and financial situations.

Choosing the right option can affect access to doctors, prescription drug coverage, out-of-pocket expenses, and overall healthcare experiences. This article provides a detailed comparison of Medicare Advantage and Original Medicare, helping readers understand their features, advantages, disadvantages, and factors to consider when making healthcare decisions.

What Is Medicare?

Medicare is a federal health insurance program primarily designed for:

- People aged 65 and older.

- Certain younger individuals with disabilities.

- Individuals with specific qualifying medical conditions.

Original Medicare is administered directly by the federal government and consists of two primary components:

Medicare Part A

Part A helps cover:

- Hospital stays

- Skilled nursing facility care

- Hospice care

- Certain home healthcare services

Many eligible individuals do not pay a monthly premium for Part A if they have sufficient work history.

Medicare Part B

Part B helps cover:

- Doctor visits

- Outpatient care

- Preventive services

- Medical equipment

- Various healthcare services

Part B generally requires a monthly premium.

Together, Part A and Part B form what is commonly known as Original Medicare.

What Is Medicare Advantage?

Medicare Advantage, also known as Medicare Part C, is an alternative way to receive Medicare benefits.

Instead of receiving coverage directly through the federal government, beneficiaries enroll in a Medicare Advantage plan offered by private insurance companies approved by Medicare.

These plans must provide at least the same level of coverage as Original Medicare but often include additional benefits.

Many Medicare Advantage plans offer:

- Prescription drug coverage

- Vision care

- Dental services

- Hearing benefits

- Wellness programs

- Fitness memberships

Because private insurers manage these plans, coverage details can vary significantly between providers.

How Original Medicare Works

Original Medicare provides flexibility in choosing healthcare providers.

Beneficiaries can generally:

- Visit any doctor who accepts Medicare.

- Use hospitals nationwide that participate in Medicare.

- Receive care without needing referrals for specialists.

This broad provider access is one of Original Medicare’s strongest advantages.

However, Original Medicare does not include routine dental, vision, or hearing coverage in most cases.

It also does not automatically include prescription drug coverage.

Many beneficiaries purchase additional plans to fill these gaps.

How Medicare Advantage Works

Medicare Advantage plans operate more like traditional private health insurance.

Most plans use provider networks that may include:

- Health Maintenance Organizations (HMOs)

- Preferred Provider Organizations (PPOs)

Depending on the plan, beneficiaries may need:

- Referrals for specialists

- Network-approved providers

- Prior authorization for certain services

In exchange for these restrictions, plans often provide additional benefits not available through Original Medicare.

Coverage Comparison

Hospital and Medical Services

Both Medicare Advantage and Original Medicare cover:

- Hospital care

- Doctor visits

- Preventive services

- Medically necessary treatment

Medicare Advantage plans must provide at least the same core benefits as Original Medicare.

Prescription Drug Coverage

Original Medicare does not automatically include prescription drug coverage.

Beneficiaries typically purchase a separate Medicare Part D plan.

Many Medicare Advantage plans include prescription drug coverage as part of the package.

This convenience appeals to many beneficiaries.

Dental Coverage

Routine dental care is generally not covered by Original Medicare.

Many Medicare Advantage plans include:

- Dental exams

- Cleanings

- X-rays

- Certain dental procedures

Coverage levels vary by plan.

Vision Coverage

Original Medicare typically does not cover routine eye exams or eyeglasses.

Many Medicare Advantage plans provide vision-related benefits.

Hearing Services

Medicare Advantage plans often include hearing exams and hearing aid assistance.

Original Medicare generally offers limited hearing-related coverage.

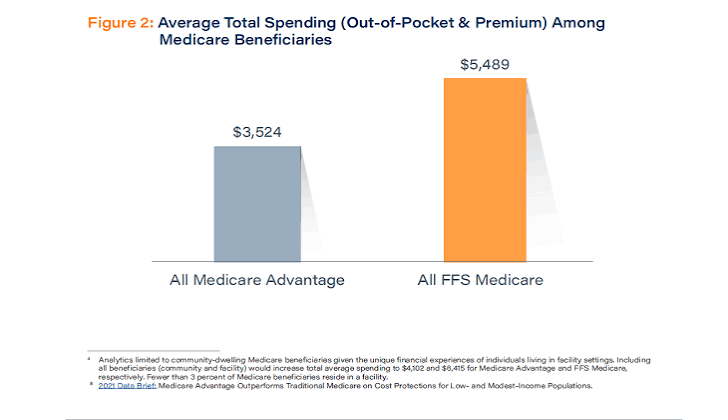

Cost Differences

Cost is often a major factor when comparing options.

Original Medicare Costs

Beneficiaries typically pay:

- Part B monthly premiums

- Deductibles

- Coinsurance

- Copayments

Because there is no annual out-of-pocket maximum, healthcare costs can potentially become significant during serious illnesses.

Many beneficiaries purchase supplemental insurance called Medigap to help cover additional expenses.

Medicare Advantage Costs

Medicare Advantage plans may include:

- Monthly premiums

- Copayments

- Deductibles

One important feature is that Medicare Advantage plans generally include an annual out-of-pocket maximum.

This cap can provide financial protection against extremely high medical expenses.

However, costs vary widely depending on the specific plan.

Provider Choice

Original Medicare

Original Medicare offers broad flexibility.

Patients can usually visit any healthcare provider nationwide who accepts Medicare.

This feature is particularly valuable for:

- Frequent travelers

- Individuals with multiple specialists

- Patients seeking maximum provider flexibility

Medicare Advantage

Most Medicare Advantage plans use provider networks.

Patients may need to:

- Stay within networks

- Obtain referrals

- Follow plan-specific requirements

Network restrictions can limit provider options but may help reduce costs.

Supplemental Insurance Considerations

Many Original Medicare beneficiaries purchase:

Medigap

Medigap policies help cover expenses such as:

- Deductibles

- Coinsurance

- Copayments

Medigap plans cannot generally be used with Medicare Advantage plans.

This distinction is important when evaluating long-term healthcare costs.

Advantages of Original Medicare

Original Medicare offers several benefits.

Greater Provider Freedom

Patients can choose from a larger pool of healthcare providers.

Nationwide Coverage

Coverage is generally available throughout the United States.

No Network Restrictions

Specialist access is often simpler.

Predictability

Coverage rules are standardized nationwide.

These factors appeal to individuals who prioritize flexibility.

Advantages of Medicare Advantage

Medicare Advantage plans also provide significant benefits.

Additional Services

Many plans include:

- Dental care

- Vision care

- Hearing services

- Wellness programs

Prescription Drug Convenience

Many plans bundle medical and prescription coverage together.

Out-of-Pocket Protection

Annual spending limits help reduce financial uncertainty.

Potentially Lower Premiums

Some plans offer low or even zero additional premiums beyond Medicare Part B.

Potential Drawbacks of Original Medicare

Original Medicare may have disadvantages.

No Out-of-Pocket Maximum

Costs can accumulate during extensive medical treatment.

Additional Plans Needed

Beneficiaries often purchase:

- Part D plans

- Medigap policies

Limited Extra Benefits

Routine dental, vision, and hearing services are generally not included.

Potential Drawbacks of Medicare Advantage

Medicare Advantage plans also have limitations.

Network Restrictions

Provider choices may be more limited.

Prior Authorization Requirements

Certain services may require approval before coverage.

Geographic Limitations

Coverage networks may vary by region.

Plan Changes

Benefits and provider networks can change annually.

Which Option Is Better?

There is no single answer because healthcare needs vary from person to person.

Original Medicare may be better for individuals who:

- Want maximum provider flexibility.

- Travel frequently.

- Prefer fewer network restrictions.

- Are comfortable purchasing supplemental coverage.

Medicare Advantage may be better for individuals who:

- Want additional benefits.

- Prefer bundled coverage.

- Seek lower upfront costs.

- Value annual out-of-pocket spending limits.

The best choice depends on healthcare usage, financial priorities, provider preferences, and lifestyle needs.

Factors to Consider Before Choosing

Before selecting a plan, consider:

Healthcare Needs

Do you visit specialists frequently?

Prescription Medications

Are prescription drugs a significant expense?

Preferred Doctors

Are your providers included in the plan’s network?

Budget

Can you afford supplemental coverage if needed?

Travel Habits

Will you need healthcare access in multiple states?

Answering these questions can help determine which option aligns best with your situation.

Conclusion

The comparison between Medicare Advantage and Medicare is one of the most important healthcare decisions many Americans face. While both options provide valuable healthcare coverage, they differ significantly in provider access, costs, benefits, and coverage structures.

Original Medicare offers flexibility, nationwide provider access, and standardized coverage, while Medicare Advantage often provides additional benefits, bundled services, and annual out-of-pocket protections. Neither option is universally better; the right choice depends on individual healthcare needs, financial goals, and personal preferences.

By carefully evaluating available plans and understanding the strengths and limitations of each option, beneficiaries can make informed decisions that support their long-term health and financial well-being.